Mortgage Calculator: Your Tool for Smarter Home Financing

Why Your Mortgage Calculator is a Game-Changer

Welcome to the age of digital wizardry, where mortgage calculators reign supreme. These savvy tools empower home buyers with the knowledge needed to navigate the labyrinth of home financing. Gone are the days of sweating over complex formulas and obscure jargon. With a mortgage calculator, you’re equipped to transform daunting figures into manageable insights. Technology has revolutionized the mortgage process, turning what was once an intimidating experience into a streamlined, user-friendly affair. Embracing this tool can save you not just money, but also a hefty dose of stress.

The Basics of Mortgage Calculators

So, what exactly is a mortgage calculator? Think of it as your financial GPS, guiding you through the maze of mortgage options. It’s a digital calculator designed to simplify the daunting task of mortgage math. These calculators take into account your loan amount, interest rate, and term, then churn out your estimated monthly payments, helping you grasp how much home you can afford. There are various types of mortgage calculators, each tailored to different needs, from simple payment calculators to advanced tools that factor in additional costs and scenarios.

Understanding Mortgage Terms

Let’s demystify some common mortgage jargon. First up is “principal,” the actual amount of money you borrow. Next, “interest” is the cost of borrowing that principal. Then we have “taxes” and “insurance,” which are additional costs rolled into your mortgage payment. Each of these components plays a crucial role in determining your overall mortgage payment. Understanding these terms helps you see beyond the monthly payment and grasp the full financial impact of your loan.

How to Use a Mortgage Calculator: A Step-by-Step Guide

Ready to dive into the world of mortgage calculators? Start by inputting your loan amount this is the sum you’re borrowing. Next, enter your interest rate, which dictates how much you’ll pay on top of the principal. Don’t forget the loan term: this is the number of years over which you’ll repay the loan. To get a more comprehensive picture, adjust for property taxes and insurance, which are often included in your monthly payment. Finally, interpret the results: your calculator will show you a breakdown of your monthly payment, including principal and interest, and potentially taxes and insurance.

The Different Types of Mortgage Calculators

Mortgage calculators aren’t one-size-fits-all. Fixed-rate mortgage calculators are the simplest, showing how a constant interest rate affects your payments over time. Adjustable-rate mortgage calculators, on the other hand, handle fluctuating rates and provide insights into how changes might impact your payments. There are also specialized calculators for specific loan types like FHA or interest-only loans, each tailored to unique financial scenarios.

Calculating Monthly Payments: The Heart of the Matter

Estimating your monthly mortgage payment is at the core of mortgage calculations. The formula considers your loan amount, interest rate, and term to determine how much you’ll pay each month. Amortization, or the gradual repayment of your loan over time, plays a key role here. Early in your loan, a larger portion of your payment goes towards interest, but as you progress, more goes towards the principal. Real-life examples illustrate how these payments evolve over the life of your mortgage.

Understanding Amortization Schedules

An amortization schedule is your roadmap for how your mortgage payments are applied. It shows each payment’s breakdown into principal and interest, and how your loan balance decreases over time. Reading this schedule can reveal how much interest you’ll pay over the life of the loan and how making extra payments can accelerate your payoff. Understanding amortization is essential for long-term financial planning and can help you see the benefits of paying down your loan more quickly.

The Role of Interest Rates in Your Calculations

Interest rates are the driving force behind your mortgage payments. Fixed interest rates remain constant throughout the loan term, providing predictability and stability. Adjustable interest rates, however, can fluctuate based on market conditions, potentially altering your payment amount. When selecting an interest rate, weigh the pros and cons of each option and consider how rate changes could impact your financial future.

Down Payments and Their Impact

Your down payment isn’t just a financial formality it significantly affects your mortgage calculation. A larger down payment reduces the amount you need to borrow, which in turn lowers your monthly payments and can even secure a better interest rate. Saving for a down payment requires strategic planning, but the benefits, including reduced mortgage insurance costs and a lower loan balance, make it worthwhile.

Property Taxes and Homeowners Insurance

Property taxes and homeowners insurance are integral to your mortgage calculation. Property taxes are typically based on the value of your home and vary by location. Homeowners insurance protects your property against damage or loss and is often required by lenders. Both of these costs are factored into your monthly mortgage payment, influencing your overall financial picture.

Using Mortgage Calculators for Budgeting

Incorporating mortgage calculations into your budgeting process is a game-changer. By understanding your mortgage payment, you can better plan your monthly budget and account for future financial changes. A mortgage calculator helps you create a realistic budget, taking into consideration potential fluctuations in your income or expenses.

Exploring Online Mortgage Calculators

Online mortgage calculators are convenient and accessible tools for anyone in the home-buying process. However, they come with pros and cons. While they simplify complex calculations and provide instant results, not all calculators are created equal. Choosing a reliable tool and comparing different calculators ensures you get accurate and useful information for your home financing needs.

Manual Calculation Methods: DIY Mortgage Math

For those who enjoy a bit of DIY, manual mortgage calculations are an option. With the right tools and formulas, you can calculate your mortgage payments without relying on online tools. This hands-on approach allows for a deeper understanding of the math behind your mortgage, though it requires careful attention to detail and accuracy.

Understanding Mortgage Points and Their Effect

Mortgage points, or discount points, are a way to prepay interest on your mortgage in exchange for a lower interest rate. Each point typically costs 1% of the loan amount and can reduce your monthly payments. Evaluating whether to buy points depends on your long-term financial goals and how long you plan to stay in your home.

Refinancing and Its Impact on Your Calculations

Refinancing your mortgage can dramatically alter your payment calculations. By securing a lower interest rate or changing your loan term, refinancing can reduce your monthly payments or shorten your loan duration. Weighing the costs and benefits of refinancing and using a calculator to evaluate potential savings is crucial in making an informed decision.

Avoiding Common Mortgage Calculation Mistakes

Mistakes in mortgage calculations can have significant financial implications. Common errors include miscalculating the loan term or interest rate, failing to account for taxes and insurance, or overlooking additional costs. Double-checking your numbers and understanding the calculation process helps avoid costly mistakes.

The Influence of Loan Term Length on Your Payments

The length of your loan term affects both your monthly payments and the total amount of interest paid over the life of the loan. Short-term mortgages typically have higher monthly payments but lower total interest costs, while long-term mortgages offer lower payments but can result in more interest over time. Choosing the right loan term aligns with your financial goals and budget.

Prepayments and Extra Payments: Boosting Your Mortgage Efficiency

Making extra payments on your mortgage can expedite the payoff process and save you money on interest. Extra payments reduce your loan balance more quickly, shortening the loan term and decreasing the total interest paid. Incorporating extra payments into your budget and understanding their impact on your mortgage efficiency enhances your financial strategy.

Adjusting for Inflation and Future Costs

Inflation and future cost increases can affect your mortgage calculations. Planning for potential rises in property taxes and insurance helps you stay prepared. Adjusting your budget to accommodate these future costs ensures that you remain financially stable throughout the life of your mortgage.

Consulting with a Mortgage Professional

When navigating complex mortgage calculations or making significant financial decisions, consulting with a mortgage professional can provide valuable guidance. These experts offer personalized advice and can help you understand the nuances of your mortgage options. Finding a qualified professional ensures you make informed decisions tailored to your unique financial situation.

Case Studies: Real-Life Examples of Mortgage Calculations

Real-life examples illustrate how mortgage calculations apply to different scenarios. By examining various cases, you can see how factors like interest rates, down payments, and loan terms impact mortgage payments. Applying these examples to your own situation helps you understand the practical implications of your mortgage choices.

Conclusion: Mastering Mortgage Calculations for Smarter Home Financing

Mastering mortgage calculations equips you with the knowledge to make smarter financial decisions. By understanding how to use mortgage calculators effectively and considering all relevant factors, you can navigate the home financing process with confidence. The benefits of accurate calculations extend beyond just securing a mortgage they empower you to manage your finances wisely.

Final Thoughts: Making Your Mortgage Work for You

Staying informed and proactive in managing your mortgage is key to achieving financial success. Accurate calculations lead to better financial outcomes and help you make smarter choices regarding your home financing. Empowering yourself with knowledge ensures that you make decisions that align with your long-term financial goals, ultimately making your mortgage work for you.

Frequently Asked Questions (FAQs)

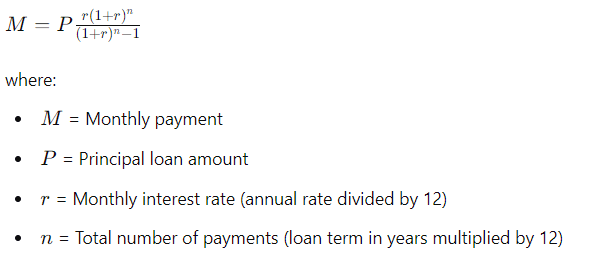

How can we calculate mortgage?

To calculate a mortgage, you need to determine the monthly payment based on the loan amount, interest rate, and loan term. The basic formula involves calculating the principal and interest components of the payment, typically using the following formula:

How do banks calculate mortgage rates?

Banks calculate mortgage rates based on several factors including the central bank’s interest rates, the borrower’s credit score, the loan-to-value ratio, and prevailing market conditions. They also consider the term of the loan and the borrower’s financial stability to determine the risk associated with lending.

What are the repayments on a 300k mortgage?

Repayments on a $300,000 mortgage depend on the interest rate and loan term. For instance, with a 4% interest rate over 30 years, the monthly payment would be approximately $1,432.25. To get the exact amount, you can use a mortgage calculator or the mortgage rate formula.

What is the mortgage rate calculation?

Mortgage rate calculation involves determining the interest rate applied to the principal balance of the loan over the term of the loan. This is typically based on the annual percentage rate (APR) which includes the interest rate and any additional fees. The formula for calculating the mortgage payment is used to determine how the rate affects the monthly payment.

How much is the mortgage payment on 400,000?

For a $400,000 mortgage, the monthly payment varies based on the interest rate and loan term. For example, with a 4% interest rate over 30 years, the monthly payment would be approximately $1,909.66. You can use a mortgage calculator to find the exact payment based on your specific terms.

What happens if I pay two extra mortgage payments a year?

Paying two extra mortgage payments a year can significantly reduce the total interest paid and shorten the loan term. This additional payment is typically applied to the principal balance, accelerating the amortization schedule and reducing the amount of interest over the life of the loan.

What is the duration of mortgage loan?

The duration of a mortgage loan typically ranges from 15 to 30 years, though some lenders offer loans with terms as short as 10 years or as long as 40 years. The loan term affects the monthly payment amount and the total interest paid over the life of the loan.

How much is the monthly payment on a 500k mortgage?

The monthly payment on a $500,000 mortgage varies with the interest rate and loan term. For example, at a 4% interest rate over 30 years, the monthly payment would be approximately $2,273.57. Use a mortgage calculator to get a precise figure based on your specific loan terms.

What are interest rates today?

Interest rates fluctuate based on economic conditions and monetary policy. As of the latest update, typical mortgage rates might range from 6% to 7% for a 30-year fixed mortgage, though rates can vary significantly based on credit score and lender. Check current rates with financial news sources or your mortgage lender for the most accurate information.

How much is a $60,000 mortgage a month?

The monthly payment on a $60,000 mortgage depends on the interest rate and loan term. For example, with a 5% interest rate over 15 years, the payment would be approximately $474.60. Use a mortgage calculator to get the exact amount based on your terms.

How much is a $400k mortgage monthly payment 25 years?

For a $400,000 mortgage over 25 years at a 4% interest rate, the monthly payment would be approximately $2,109.44. This figure can vary based on the exact interest rate and any additional fees.

What is 5 percent of 600k?

5 percent of $600,000 is $30,000. This can be calculated by multiplying $600,000 by 0.05.

What is monthly mortgage on 250k?

The monthly mortgage payment on a $250,000 loan depends on the interest rate and term. For a 30-year loan at 4%, the payment would be approximately $1,193.54. Adjust the rate and term to find the exact payment for your specific situation.

How much deposit do you need for a mortgage in USA?

The standard deposit, or down payment, required for a mortgage in the USA is typically 20% of the purchase price. However, many lenders offer options with lower down payments, such as 3% to 5% for conventional loans or even less for certain government-backed loans.

How much is a downpayment on a house in California?

In California, the down payment for a house generally ranges from 5% to 20% of the purchase price. For a $500,000 home, this means a down payment could be between $25,000 and $100,000, depending on the loan type and lender requirements.

How much is a $200,000 mortgage payment for 30 years?

For a $200,000 mortgage with a 4% interest rate over 30 years, the monthly payment would be approximately $954.83. This amount includes both principal and interest.

What income do you need for a 700K mortgage in Canada?

To qualify for a $700,000 mortgage in Canada, income requirements vary based on the interest rate, down payment, and other financial factors. Typically, a household income of approximately $130,000 to $150,000 might be required, depending on the lender’s criteria and debt service ratios.

How much is a $500,000 mortgage payment for 30 years?

For a $500,000 mortgage with a 4% interest rate over 30 years, the monthly payment would be approximately $2,273.57. This calculation includes principal and interest.

How much is the mortgage on $150,000?

The mortgage payment on a $150,000 loan depends on the interest rate and term. For example, with a 5% interest rate over 30 years, the monthly payment would be approximately $805.23.

What is repayment on $400,000 mortgage?

Repayment on a $400,000 mortgage depends on the interest rate and loan term. For instance, with a 4% interest rate over 30 years, the monthly payment would be around $1,909.66. Use a mortgage calculator to get precise repayment figures based on your specific terms.

How much mortgage can I get with $70,000 salary in Canada?

With a $70,000 annual salary in Canada, the mortgage amount you can qualify for varies based on your financial situation and current interest rates. Generally, lenders use a debt service ratio to determine affordability. You might be able to secure a mortgage of approximately $350,000 to $450,000, depending on other financial factors.

What will be the monthly payment on a $75,000 30 year home mortgage at 1% interest per month?

For a $75,000 mortgage over 30 years at a 1% interest rate per month (which translates to an annual rate of 12%), the monthly payment would be approximately $655.64. Use a mortgage calculator for precise calculations based on your specific interest rate.

What is the mortgage on $250,000?

The monthly mortgage payment on a $250,000 loan varies with the interest rate and loan term. For a 30-year mortgage at 4%, the payment would be around $1,193.54. Adjust the rate and term to find the exact payment for your specific situation.