Why You Should Use a Car Payment Calculator

Navigating the world of car financing can feel like trying to assemble a jigsaw puzzle blindfolded. But here’s the kicker: you don’t have to stumble into financial quicksand. A car payment calculator is your secret weapon for cutting through the noise and avoiding any wallet-busting surprises.

The Importance of Financial Planning Before Buying a Car

Before you dive into test drives and heated negotiations, it’s crucial to know what you can actually afford. Financial planning is about making sure your future self doesn’t resent your present self for choosing leather seats over groceries.

How Car Payment Calculators Save You from Costly Mistakes

A car payment calculator takes the guesswork out of the equation. It lets you see the full picture: monthly payments, total interest, and how much that shiny new ride will truly cost you. Spoiler alert: it’s probably more than you think.

What Is a Car Payment Calculator?

You might think a car payment calculator is some arcane tool, but it’s actually as straightforward as it gets💵assuming you know what numbers to punch in.

Breaking Down the Basics: How It Works

Think of it as a math tutor for grown-ups. A car payment calculator takes basic inputs like the loan amount, interest rate, and loan term to spit out your expected monthly payment. Magic? Not quite, but it feels close.

Key Variables: What You Need to Input for Accurate Results

To make sure you get an accurate figure, you’ll need to enter the loan amount, interest rate, loan term, and any down payment or trade-in value. Forget to include these, and you might be in for a nasty surprise when your first bill arrives.

The Benefits of Using a Car Payment Calculator

Avoiding Financial Surprises: Know What You’ll Pay

No one likes being blindsided💵especially by money. By using a car payment calculator, you’ll know exactly what to expect each month, down to the penny.

Budgeting Made Easy: Aligning Your Car Payments with Your Income

Buying a car should feel like a victory, not a financial fiasco. A calculator helps you ensure that your car payment fits snugly into your budget, rather than exploding it.

Saving Time and Stress: No More Guesswork at the Dealership

Tired of sweating through negotiations? Arrive armed with your car payment calculator results, and you can negotiate with confidence💵or at least avoid that nervous laugh when they show you the financing options.

Taking in the Math Behind Car Payments

Principal, Interest, and Term Length: The Holy Trinity

Your car payment is determined by three key factors: principal (the loan amount), interest (the lender’s cut), and term length (how long you’ll be paying). Get one wrong, and your monthly payment will balloon faster than you can say “extended warranty.”

How Loan Terms Affect Your Monthly Payment

Longer loan terms lower your monthly payment but rack up more interest in the long run. Shorter terms do the opposite💵higher payments but less time paying. It’s all about finding that sweet spot.

Interest Rates Explained: Fixed vs. Variable Rates

Fixed rates stay the same for the life of your loan, while variable rates fluctuate with the market. Fixed offers stability; variable offers potential savings… and stress.

The Impact of Your Down Payment on Your Monthly Cost

A bigger down payment lowers your principal, meaning less interest to pay and a lower monthly cost. It’s the classic case of paying more now to pay less later.

How to Use the Car Payment Calculator Like a Pro

Step-by-Step Guide to Entering the Right Information

Start with the basics: enter the vehicle’s price, your down payment, the loan term, and the interest rate. Voila! Your monthly payment pops up, as if by magic.

Common Mistakes to Avoid When Calculating Payments

Don’t forget the fine print! Taxes, fees, and insurance can all throw off your calculations if not included. Skip these at your peril.

What If You’re Leasing? Adjusting the Calculator for Leasing Terms

Leasing has different variables: the capitalized cost, residual value, and money factor. Be sure to switch the calculator mode accordingly to avoid sticker shock when your lease bill arrives.

Maximizing Your Savings with the Car Payment Calculator

Strategies for Lowering Monthly Payments

To keep your monthly payment down, increase your down payment, opt for a shorter loan term, or find a lower interest rate. Simple math with significant savings.

How to Shorten Your Loan Term Without Breaking the Bank

Consider making extra payments toward the principal each month. A little extra can shave years💵and interest💵off your loan.

Refinancing: Can It Lower Your Payment Further?

If you’re stuck with a high interest rate, refinancing could help. Just be sure the new loan terms are better, not worse.

Down Payments: How Much Should You Put Down?

The Magic Number: Why 20% Isn’t Just a Myth

A 20% down payment isn’t just arbitrary; it significantly reduces your loan amount, interest, and monthly payment. Consider it your golden ticket to affordable car ownership.

Smaller Down Payment, Bigger Monthly Payments: Is It Worth It?

Less money down means more money in your pocket today💵but you’ll pay for it in higher monthly payments. Weigh your short-term needs against long-term costs.

Zero Down: The Pros and Cons of Putting Nothing Upfront

Zero down payments sound appealing, but they lead to higher interest costs and monthly payments. It’s a gamble💵one you might regret after the initial thrill wears off.

Loan Term Length: Should You Stretch It Out?

Short-Term Loans: Higher Payments but Less Interest

Want to pay less overall? A shorter loan term results in higher monthly payments but fewer total interest payments.

Long-Term Loans: Lower Payments but at What Cost?

Lower monthly payments may feel like a win, but long-term loans stretch out the interest payments, meaning you’ll pay more over time.

How to Find the Sweet Spot Between Affordability and Cost

The trick is finding the balance. Calculate your payments for various loan terms, and see where affordability meets minimal interest.

Credit Score and Your Car Payment: The Connection

How Your Credit Score Affects Interest Rates

A better credit score means a lower interest rate. Lenders reward good credit with better terms, while bad credit means higher costs.

Improving Your Credit Before Applying for a Car Loan

If your credit’s in the dumps, consider boosting it before buying a car. A few points can mean a significant savings on interest.

Bad Credit? How to Navigate Higher Interest Rates

If your credit is poor, you might still get a loan💵but at a cost. Shop around, and consider a co-signer or making a larger down payment to offset the higher rate.

Hidden Costs in Car Payments: Watch Out!

Fees, Insurance, and Taxes: The Costs That Add Up

Beyond the car and the interest, you’ve got fees, insurance, and taxes. Don’t forget to account for these in your calculations, or your “affordable” car might suddenly seem less so.

The Fine Print: What Car Dealerships Don’t Always Tell You

Dealerships love to bury additional costs in the fine print. Read everything before you sign💵trust me.

The True Cost of Ownership: Factoring in Maintenance and Repairs

Your monthly car payment is just the beginning. Regular maintenance, unexpected repairs, and depreciation all contribute to your car’s true cost of ownership.

How Different Types of Loans Affect Your Payment

Traditional Auto Loans vs. Dealer Financing: What’s the Difference?

Dealerships often offer in-house financing, but it’s not always the best deal. Compare it to traditional auto loans to make sure you’re getting the best rate.

Balloon Payments: Low Monthly Payments, Big End Costs

Balloon loans offer tantalizingly low monthly payments, but beware: the final “balloon” payment can be massive. Make sure you’re prepared to pay it.

Personal Loans for Cars: A Good Idea?

Using a personal loan for a car purchase can work in some cases, but typically, auto loans offer better terms.

Leasing vs. Buying: Which Makes More Sense for You?

How Lease Payments Differ from Loan Payments

Leasing typically results in lower monthly payments compared to buying, but you’re essentially renting the car for a set period without owning it.

Understanding Residual Value and Its Impact on Your Lease

Residual value is the car’s expected worth at the end of your lease. The higher the residual value, the lower your lease payments.

The Long-Term Financial Impact of Leasing vs. Owning

While leasing can be cheaper in the short term, ownership can offer more value over time. It’s a trade-off between flexibility and long-term cost.

Calculating Car Affordability: How Much Car Can You Really Afford?

Why It’s Important to Factor in Total Cost, Not Just Monthly Payments

A low monthly payment doesn’t mean you can afford the car. Consider the total cost, including interest, fees, and other expenses.

The 20/4/10 Rule: A Simple Formula for Smart Car Buying

The 20/4/10 rule suggests a 20% down payment, a loan term of no more than four years, and car expenses that don’t exceed 10% of your gross monthly income.

Avoiding the Pitfalls of Buying More Car Than You Need

It’s easy to get carried away with fancy features, but overspending on a car can have serious long-term financial consequences.

The Role of Trade-Ins in Your Car Payment

How Trade-Ins Affect Your Loan Amount and Monthly Payments

Trading in your old car reduces your loan amount and can lower your monthly payments. Make sure you get a fair trade-in value to maximize your savings.

When to Trade in Your Old Car: Timing is Everything

The value of your trade-in decreases with every mile. The key is to trade it in before it depreciates too much, while it’s still a valuable asset.

Should You Sell Your Car Privately for More Cash?

Selling your car privately can net you more cash than a trade-in, but it requires more effort. The extra money may be worth the hassle.

How Interest Rates Fluctuate Based on Loan Terms

Understanding Market Trends: When Is the Best Time to Get a Car Loan?

Interest rates can vary based on the economy and market trends. Watch for rate drops and consider locking in a loan when rates are favorable.

Why Dealer Interest Rates Might Be Higher Than You Think

Dealerships sometimes inflate interest rates to make up for lower sticker prices. Always compare dealer financing to outside lenders to make sure you’re getting a fair deal.

How to Lock in the Best Rate for Your Situation

To secure the best interest rate, shop around, check your credit score, and time your loan application to align with favorable market conditions.

Refinancing Your Car Loan: Is It Worth It?

When and Why to Refinance Your Auto Loan

If interest rates drop or your financial situation improves, refinancing could save you money by lowering your interest rate or monthly payment.

How Refinancing Can Lower Your Monthly Payment or Interest Rate

Refinancing can reduce your interest rate and, in turn, your monthly payment. Just make sure the new loan term doesn’t extend too far.

Refinancing Pitfalls: What to Watch Out For

Be wary of extending your loan term too long when refinancing. While it might lower your payment, you could end up paying more in interest over the life of the loan.

The Impact of Inflation on Car Payments in 2024

Rising Prices: How Inflation Affects Car Loan Interest Rates

Inflation can drive up interest rates, making car loans more expensive. Understanding inflation trends can help you time your purchase and loan agreement.

Planning for Economic Uncertainty: Fixed vs. Variable Rates

In times of economic uncertainty, a fixed-rate loan offers stability. Variable rates, while potentially lower initially, can rise unpredictably.

Should You Lock In a Loan Now or Wait?

If interest rates are rising, locking in a loan sooner might save you money. However, waiting for a rate drop could also work in your favor💵if you’re willing to take the risk.

Case Study: Real-Life Examples of Car Payment Calculations

Example 1: A $20,000 Loan at 3% Interest for 5 Years

A $20,000 loan at 3% for five years would result in a manageable monthly payment of around $360. This is a realistic example for many buyers looking for a practical vehicle.

Example 2: A $35,000 Loan with No Down Payment for 7 Years

A higher loan amount and no down payment would push monthly payments over $500, and the extended term adds significant interest to the total cost.

Example 3: Leasing a $30,000 Car vs. Buying It Outright

Leasing the same $30,000 car would result in lower monthly payments than buying, but you’d have no equity at the end. Buying outright costs more upfront but provides ownership.

Using the Car Payment Calculator to Plan for Future Purchases

How to Use the Calculator for Trade-Ins and Upgrades

Planning to upgrade in a few years? The calculator helps you see how trade-ins affect future payments, ensuring your next car purchase is equally savvy.

Planning for an Electric Vehicle: Are Payments Higher or Lower?

Electric vehicles (EVs) often come with higher sticker prices but lower fuel costs. Use the calculator to weigh these factors and determine if an EV fits your budget.

Future-Proofing Your Payments: Preparing for Interest Rate Hikes

If you’re concerned about rising interest rates, locking in a lower rate now could save you money in the future. Plan ahead to stay ahead.

Tips for Lowering Your Monthly Payment Without Stretching Your Budget

Negotiating with Dealers: How to Get the Best Deal

Walk into the dealership armed with knowledge. Negotiating the price, interest rate, and trade-in value can help lower your monthly payment without stretching your budget.

Timing Your Purchase for Seasonal Discounts

Dealerships often offer discounts at the end of the year or during holiday sales. Timing your purchase for these events can result in significant savings.

Should You Buy a Certified Pre-Owned Car Instead?

Certified pre-owned cars offer the reliability of a new car without the new car price. This can be a savvy way to lower your payment without sacrificing quality.

Final Thoughts: Making the Car Payment Calculator Work for You

Why Every Buyer Should Use a Car Payment Calculator Before Shopping

Whether you’re buying new, used, or leasing, a car payment calculator is an invaluable tool. It saves time, money, and helps you make informed decisions.

How to Combine Budgeting Tools for Maximum Savings

Pair your car payment calculator with other budgeting tools to maximize your savings. Knowing what you can afford puts you in the driver’s seat, both literally and financially.

Ready to Shop? Your Next Steps Toward a Smarter Car Purchase

Now that you’ve got the numbers, it’s time to hit the dealerships with confidence. Stick to your budget, negotiate wisely, and drive off with a payment plan that works for you.

Call to Action: Try Our Car Payment Calculator Today

Get Started Now: Calculate Your Car Payment in Minutes

Ready to crunch the numbers? Use our car payment calculator to get started on your journey toward a no-surprises car purchase.

Ready to Buy? Use Your Results to Secure the Best Deal at the Dealership

Once you’ve got your payment estimate, take it to the dealership and use it as your starting point. Negotiating just got a whole lot easier.

People Also Ask

How to calculate APR on a car loan?

The APR (Annual Percentage Rate) is calculated by combining the interest rate and any fees or costs associated with the loan into an annualized percentage. To calculate APR on a car loan, use this formula:

APR Formula:

You can also use online APR calculators to make the process simpler.

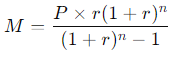

How much is the monthly payment on a $32,000 car loan?

To determine the monthly payment on a $32,000 car loan, you need to know the interest rate, loan term, and whether it is a simple interest loan or compound interest loan. Use the loan amortization formula:

Where:

- M is the monthly payment

- P is the principal loan amount ($32,000)

- r is the monthly interest rate (annual rate divided by 12)

- n is the number of payments (loan term in months)

How to calculate loan payments with interest?

You can calculate loan payments with interest using the formula mentioned above. Break down the annual interest rate into monthly installments and apply it across the duration of the loan. The payment includes both the principal and the interest over time.

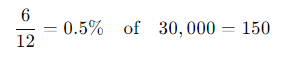

What is 6% interest on a $30,000 loan?

To find the annual interest amount on a $30,000 loan at 6% interest:

Interest Formula:

How much would a $5000 loan cost per month?

The monthly cost for a $5,000 loan depends on the interest rate and loan term. Using the loan payment formula and plugging in the numbers will give you the exact monthly payment.

What is the formula for monthly payment?

The formula to calculate monthly payments for a loan is:

Where:

- M is the monthly payment

- P is the loan principal

- r is the monthly interest rate

- n is the number of payments

What is a good interest rate for a car?

A good interest rate for a car loan depends on your credit score and market conditions. As of 2024, a good interest rate would typically range from 3% to 5% for borrowers with excellent credit. For those with lower credit scores, rates may be higher.

How long is 84 months?

84 months is equivalent to 7 years.

What is the car loan interest rate?

Car loan interest rates vary depending on the borrower’s creditworthiness, the loan term, and the lender. Interest rates can range from as low as 2% to upwards of 15% for subprime borrowers.

How much interest will I pay per month?

The monthly interest on a car loan can be calculated by multiplying the outstanding principal by the monthly interest rate. For instance, if the annual interest rate is 6% and the loan amount is $30,000, the monthly interest for the first month would be:

So the interest for the first month is $150.

Who has the lowest auto loan rates?

The lowest auto loan rates are often offered by credit unions, online banks, and some local banks. Rates vary based on credit scores, loan terms, and promotions.

Can you pay off a car loan early?

Yes, you can typically pay off a car loan early, but you should check with your lender to see if there are any prepayment penalties or fees for doing so.

What is the formula for a car loan?

The formula for calculating a car loan payment is the loan amortization formula:

This includes both the principal and interest payments over the loan term.

{kind=link}